Invest

Invest

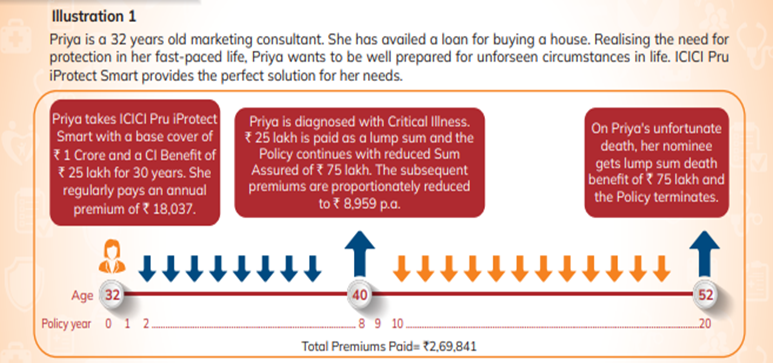

How Does the plan work

-

Decide the amount of protection you need

-

Enhance your policy by selecting from the additional benefits

-

Choose your policy term and premium payment term