Invest

Invest

Fundamental Outlook

| Particulars | FY19 | FY20 | FY21E | 4 Year CAGR(FY16-FY20) | FY22E | FY23E | FY24E | 3 Year CAGR (FY21-FY24E) |

|---|---|---|---|---|---|---|---|---|

| Net Sales | 8117.7 | 8787.9 | 5249 | 10 | 8203 | 11390.5 | 13565.6 | 37 |

| EBITDA | 554.1 | 1211.8 | 555 | - | 990.2 | 1824.2 | 2186.1 | 58 |

| RoCE (%) | 10.7 | 10.2 | 8.9 | - | 4.1 | 22.5 | 26 | - |

| RoE (%) | 22.5 | -15.3 | -25.5 | - | -4.3 | 14.1 | 15.2 | - |

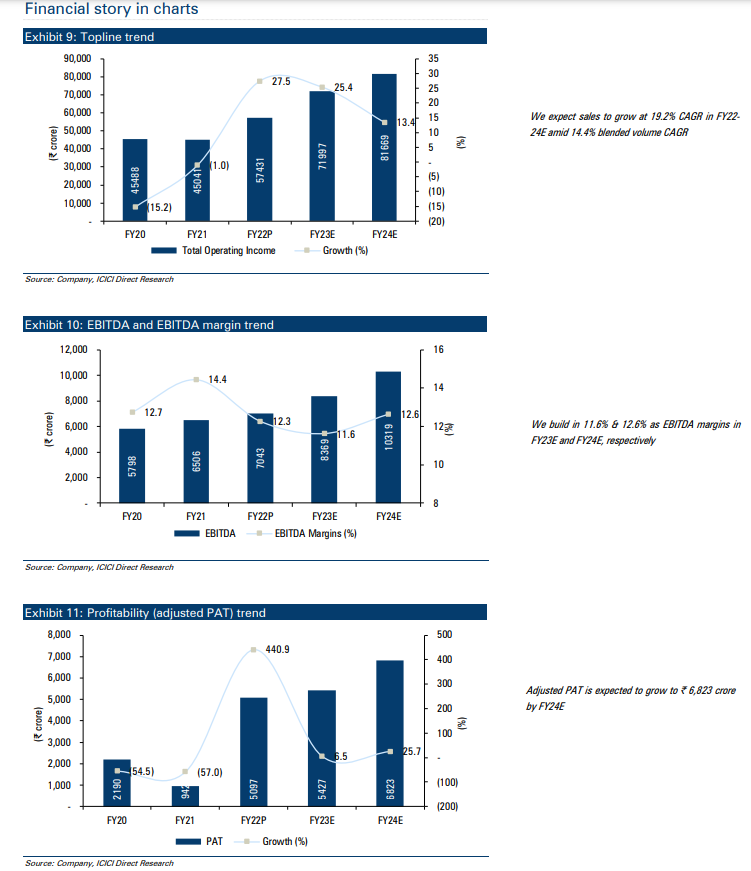

| Particulars | FY19 | FY20 | FY21 | FY22P | 5 year CAGR (FY17-22) | FY23E | FY24E | 2 year CAGR (FY22-24E) |

|---|---|---|---|---|---|---|---|---|

| Net Sales | 53,614.0 | 45,487.8 | 45,041.0 | 57,431.0 | 5.4 | 71,996.8 | 81,668.9 | 19.2 |

| EBITDA | 6,639.6 | 5,798.0 | 6,506.1 | 7,042.9 | 9.3 | 8,658.7 | 10,618.0 | 22.8 |

| EBITDA Margins (%) | 12.4 | 12.7 | 14.4 | 12.3 | - | 12.0 | 13.0 | - |

| Net Profit | 4,796.1 | 1,330.4 | 268.6 | 4,932.4 | 6.2 | 5,677.9 | 7,119.9 | 20.1 |

| Adjusted Net Profit | 4,818.6 | 2,190.4 | 942.5 | 5,097.5 | 9.6 | 5,677.9 | 7,119.9 | 18.2 |

| EPS (₹) | 41.56 | 11.2 | 2.3 | 41.3 | - | 47.6 | 59.7 | - |

| P/E | 26.6 | 95.9 | 475.2 | 25.9 | - | 22.5 | 17.9 | - |

| RoNW (%) | 14.1 | 6.4 | 2.7 | 13.1 | - | 13.1 | 14.7 | - |

| RoCE (%) | 12.3 | 8.8 | 9.5 | 9.3 | - | 11.3 | 13.5 | - |

|

Category of Shareholders |

% of Share Capital |

|---|---|

|

Antfin ( Netherlands) Holding B.V. |

29.6% |

|

SAIF III Mauritius Company Limited |

12.1% |

|

Vijay Shekhar Sharma |

9.6% |

|

Alibaba.com Singapore E-Commerce Private Limited |

7.2% |

|

SAIF Partners India IV Limited |

5.1% |

|

BH International Holdings |

2.8% |

|

SVF Panther (Cayman) Limited |

1.3% |

| Particulars | FY19 | FY20 | FY21 | FY22P | 5 year CAGR (FY17-22) | FY23E | FY24E | 2 year CAGR (FY22-24E) |

|---|---|---|---|---|---|---|---|---|

| Net Sales | 53,614.0 | 45,487.8 | 45,041.0 | 57,431.0 | 5.4 | 71,996.8 | 81,668.9 | 19.2 |

| EBITDA | 6,639.6 | 5,798.0 | 6,506.1 | 7,042.9 | 9.3 | 8,658.7 | 10,618.0 | 22.8 |

| EBITDA Margins (%) | 12.4 | 12.7 | 14.4 | 12.3 | - | 12.0 | 13.0 | - |

| Net Profit | 4,796.1 | 1,330.4 | 268.6 | 4,932.4 | 6.2 | 5,677.9 | 7,119.9 | 20.1 |

| Adjusted Net Profit | 4,818.6 | 2,190.4 | 942.5 | 5,097.5 | 9.6 | 5,677.9 | 7,119.9 | 18.2 |

| EPS (₹) | 40.2 | 11.2 | 2.3 | 41.3 | - | 47.6 | 59.7 | - |

| P/E | 26.6 | 95.9 | 475.2 | 25.9 | - | 22.5 | 17.9 | - |

| RoNW (%) | 14.1 | 6.4 | 2.7 | 13.1 | - | 13.1 | 14.7 | - |

| RoCE (%) | 12.3 | 8.8 | 9.5 | 9.3 | - | 11.3 | 13.5 | - |

Trading portfolio allocation

For example: The ‘Momentum Picks’ product carries 2 intraday recommendations. It is advisable to allocate equal amount to each recommendation

We/I, Dharmesh Shah, Nitin Kunte, Ninad Tamhanekar, Pabitro Mukherjee, Vinayak Parmar Research Analysts, authors and the names subscribed to this report, here by certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensations, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. We confirmed that above mentioned Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months and do not serve as an officer, director or employee of the companies mentioned in the report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products.

ICICI Securities is Sebi registered stock broker, merchant banker, investment adviser, portfolio manager and Research Analyst. ICICI Securities is registered with Insurance Regulatory Development Authority of India Limited (IRDAI) as a composite corporate agent and with PFRDA as a Point of Presence. ICICI Securities Limited Research Analyst SEBI Registration Number – INH000000990. ICICI Securities Limited SEBI Registration is INZ000183631 for stock broker. ICICI Securities is a subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

Recommendation in reports based on technical and derivative analysis centre on studying charts of a stocks price movement, outstanding positions, trading volume etcas opposed to focusing on a companys fundamentals and, as such, may not match with the recommendation in fundamental reports. Investors may visit icicidirect.com to view the Fundamental and Technical Research Reports. Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.

ICICI Securities Limited has two independent equity research groups: Institutional Research and Retail Research. This report has been prepared by the Retail Research. The views and opinions expressed in this document may or may not match or may be contrary with the views, estimates, rating, target price of the Institutional Research.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of interest at the time of publication of this report.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report.

Since associates of ICICI Securities and ICICI Securities as a entity are engaged in various financial service businesses, they might have financial interests or actual/ beneficial ownership of one percent or more or other material conflict of interest various companies including the subject company/companies mentioned in this report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction